The Shifting Ground Beneath Your California Home

You’ve probably felt it – that little jolt, or maybe you’ve just seen a crack forming in the wall. For homeowners in California, the thought of foundation damage can send a shiver down your spine. Our state, with its active seismic zones, vast and varied soils, and sometimes dramatic weather shifts, presents a unique set of challenges. It’s not just a house sitting on dirt; it’s a house sitting on *California* dirt. And that dirt can have a mind of its own.

Foundation problems are more than just an eyesore. They can threaten the structural integrity of your home, devalue your property, and cost a fortune to fix. So, it’s natural to wonder: does your home insurance policy have your back if the ground decides to get restless? The short answer is sometimes. The real answer is, well, a lot more complicated.

What Exactly Counts as Foundation Damage?

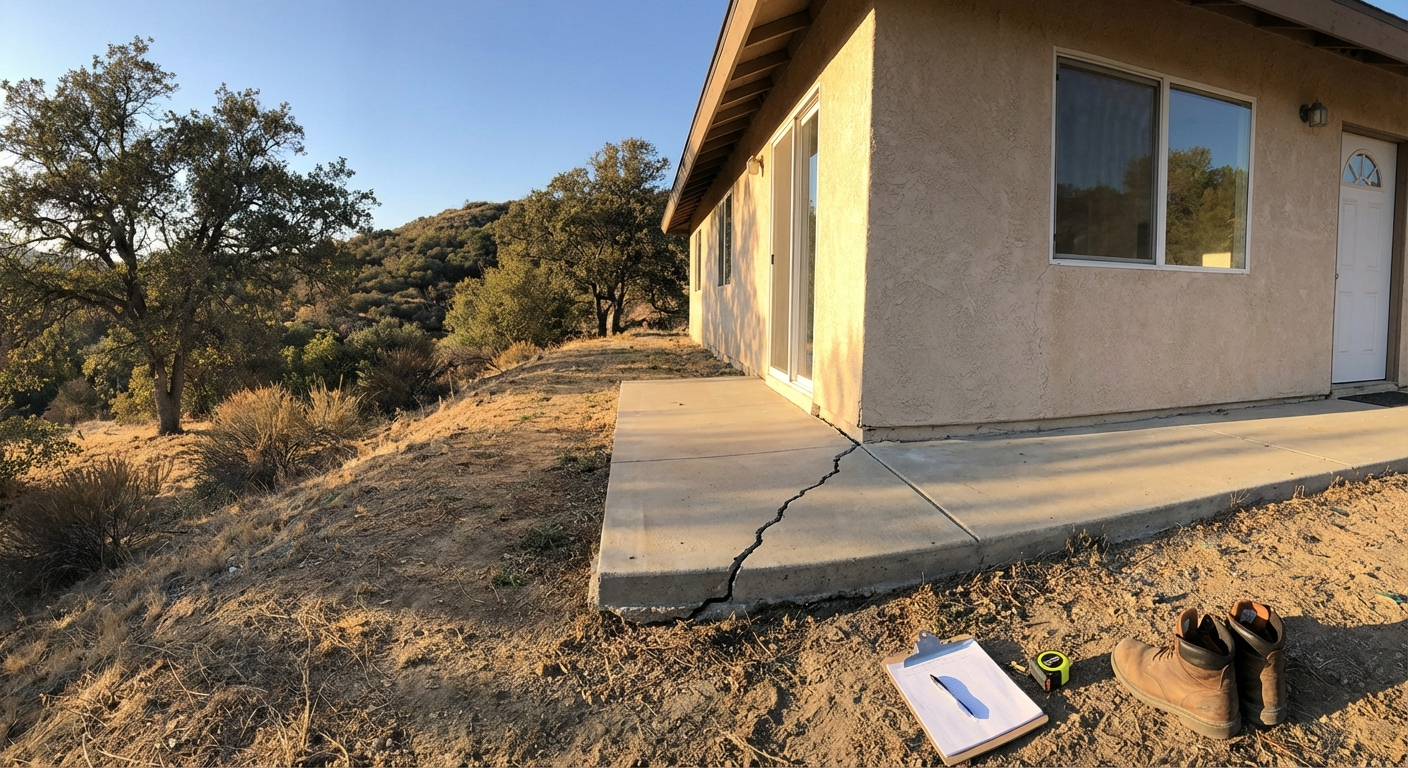

Before we talk about insurance, let’s get clear on what we’re actually talking about. Foundation damage isn’t just one thing. It could be anything from minor cracks in a concrete slab to significant sinking or shifting of the entire structure.

Many things can cause these issues here in California. Expansive clay soils, common in places like the San Fernando Valley or parts of the Inland Empire, soak up water and swell, then shrink when they dry out. This constant expansion and contraction puts immense stress on foundations. Then there’s the obvious one: earthquakes. Even small tremors can create hairline fractures that worsen over time.

But wait — it’s not always about the earth moving. Poor drainage around your home can let water seep under the slab, eroding the soil beneath. Sometimes, a leaky pipe underground goes unnoticed for months, slowly washing away the very support your house needs. Tree roots, though beautiful, can also be destructive, growing under and against your foundation, causing uplift or cracks.

Does Your Standard Policy Cover Foundation Problems? Here’s the Catch.

This is where most people get confused. Most standard home insurance policies – often called HO-3 policies – are “open perils” for your dwelling. That means they cover everything *unless* specifically excluded. And foundation damage? Often, it falls right into those exclusions.

Generally, your policy is designed to cover “sudden and accidental” damage. Think of a pipe bursting and flooding your basement – that’s sudden. A car crashing into your living room – definitely accidental. But foundation issues often develop slowly, over years. That’s a big difference.

Let’s break down some common causes and how they stack up against your policy:

Earthquakes and Earth Movement

You’d think living in California, earthquake damage would be a given, right? Not so much. Standard home insurance policies *never* cover earthquake damage. This includes damage to your foundation caused by seismic activity. If you live in Ventura County, near a fault line, or anywhere in the state, really, and want protection against earthquakes, you’ll need a separate earthquake insurance policy. These are typically offered through the California Earthquake Authority (CEA) or private insurers. It’s an extra cost, yes, but for many, it’s a peace-of-mind investment that makes sense.

Which brings up something most people miss: “earth movement” is a broad exclusion. This doesn’t just mean earthquakes. It often includes landslides, mudslides, and even the settling or shifting of soil over time. So, if your home’s foundation starts sinking because the soil beneath it slowly eroded away from years of poor drainage – that’s likely an “earth movement” exclusion at play, and your standard policy probably won’t pay for repairs.

Water Damage: Sudden vs. Slow Leaks

This is a tricky one. If a water pipe *inside* your house suddenly bursts and the resulting flood compromises your foundation, that sudden damage is generally covered. Your policy would likely pay to fix the pipe and repair the foundation damage directly caused by that specific incident.

But here’s the thing. What if you have a slow, persistent leak from a pipe under your slab that goes undetected for months or even years? That constant trickle can slowly wash away the soil supporting your foundation, causing it to crack or sink. Most policies consider this “gradual damage” or damage due to “wear and tear,” or even “neglect.” And that’s usually not covered. Insurers expect you, the homeowner, to maintain your property and address small issues before they become big ones.

Expansive Soils and Drought/Flood Cycles

The clay soils found across much of California, from the Central Valley to the hills around Los Angeles, are notorious for their expansive properties. During dry spells, like the droughts we’ve seen, these soils shrink. When the rains come, they swell dramatically. This constant movement puts tremendous stress on foundations.

Honestly, damage from this kind of soil movement is almost always excluded under the general “earth movement” clause. Your policy isn’t designed to cover the natural, ongoing processes of the earth, even if aggravated by weather patterns.

Tree Roots and Poor Construction

A beautiful oak tree can add so much character to your property. But if its roots are aggressively growing towards your home, they can push against your foundation, causing cracks and shifting. Generally, damage caused by tree roots is considered a maintenance issue, and thus, not covered by your standard home insurance policy. You’re expected to manage the landscaping around your home to prevent such problems.

What if the foundation issues stem from the original construction being shoddy? If the house was built poorly, leading to foundation problems down the road, your home insurance policy won’t cover that either. That’s typically a matter for the builder’s warranty (if it’s still active) or a lawsuit against the builder. It’s not an insured peril.

The Value of an Expert Opinion

It’s easy to feel overwhelmed by all these nuances. This is exactly why talking to someone who understands the intricacies of California insurance is so important. Someone like Karl Susman at Los Angeles Home Coverage, CA License #OB75129, has spent years helping California homeowners make sense of their options. He knows the local landscape, the common issues, and how different policies respond.

You don’t want to find out you’re underinsured or have the wrong coverage *after* a problem strikes. Knowing your policy inside and out – or having someone explain it to you in plain English – can save you heartache and serious money down the line.

Ready to understand your home insurance better and make sure your foundation is as protected as it can be? Get a personalized quote and speak with an expert today.

Get Your Home Insurance Quote Here

What to Do if You Suspect Foundation Damage

Let’s say you notice a new crack in your stucco, or a door that suddenly doesn’t close right. What’s your first move?

1. **Document Everything:** Take photos and videos. Keep a log of when you first noticed the damage and how it progresses.

2. **Contact Your Insurer (and Your Agent):** Report the potential damage right away. Be honest about what you’ve observed. Your agent can help you understand if it’s even worth filing a claim, given your policy’s exclusions.

3. **Get Professional Assessments:** Before you start any repairs, get an opinion from a structural engineer or a foundation repair specialist. They can diagnose the cause and extent of the damage. This documentation will be invaluable if you do file a claim.

4. **Mitigate Further Damage:** Do what you can to prevent the problem from getting worse. If it’s a drainage issue, fix the drainage. If it’s a leaky pipe, get it repaired. Your policy often requires you to take reasonable steps to prevent further loss.

Navigating the California Insurance Market

The insurance market in California has been pretty turbulent lately. Premiums jumped 40% between 2022 and 2024 for some policies, and some major carriers like State Farm and Farmers have even pulled back from offering new policies in certain areas. This makes finding good coverage, especially for unique California risks, tougher than ever.

That’s why a local expert’s perspective is invaluable. They understand how things like the FAIR Plan interact with standard policies, or how changes driven by Prop 103 might affect your options. It’s not just about getting a policy; it’s about getting the *right* policy for your specific home in your specific part of California.

FAQ: Foundation Damage and Home Insurance in CA

Q: Will my home insurance cover foundation repair if a tree falls on my house?

A: Yes, if a tree falls due to a covered peril (like a windstorm) and directly damages your foundation, your standard policy would likely cover the repair. This falls under “sudden and accidental” damage caused by a covered event.

Q: What’s the difference between “settling” and “shifting” in terms of coverage?

A: “Settling” refers to the natural, gradual movement of a house over time as it adjusts to its foundation and the soil. This is almost never covered. “Shifting” often implies more dramatic, sudden movement, which *might* be covered if it’s caused by a sudden, accidental, and covered peril, but often it’s still excluded under “earth movement.” It’s a fine line, and often debated.

Q: Are sinkholes covered by California home insurance?

A: Most standard home insurance policies in California do not specifically cover sinkholes, as they fall under the general “earth movement” exclusion. Some specialized policies or endorsements might offer this protection, but it’s not standard.

Q: How much does it typically cost to fix foundation damage in California?

A: Foundation repair costs vary wildly depending on the extent and type of damage. Minor crack repairs might be a few thousand dollars, but significant underpinning or slab replacement can easily run into the tens of thousands, or even hundreds of thousands for severe issues. It’s a major expense.

Q: Can I get an endorsement to cover expansive soil damage?

A: While some insurers might offer specific endorsements for certain types of perils, coverage for damage explicitly caused by the natural expansion and contraction of soil is extremely rare, if not impossible, to find on a standard policy. It’s generally considered an inherent risk of building on certain soil types.

Thinking Ahead

Protecting your home’s foundation in California isn’t just about reacting to problems. It’s about being proactive. It means understanding your property’s unique risks, maintaining good drainage, and most importantly, making sure you have the right insurance coverage in place *before* disaster strikes. Don’t leave your biggest investment exposed to the unpredictable nature of our beautiful, sometimes shaky, state.

For personalized advice on navigating your home insurance options in California, including understanding foundation damage coverage, reach out to Karl Susman at Los Angeles Home Coverage, CA License #OB75129. You can call him directly at (877) 411-5200 or get started online.

Get Your Home Insurance Quote Today

This article is for informational purposes only and does not constitute financial advice.